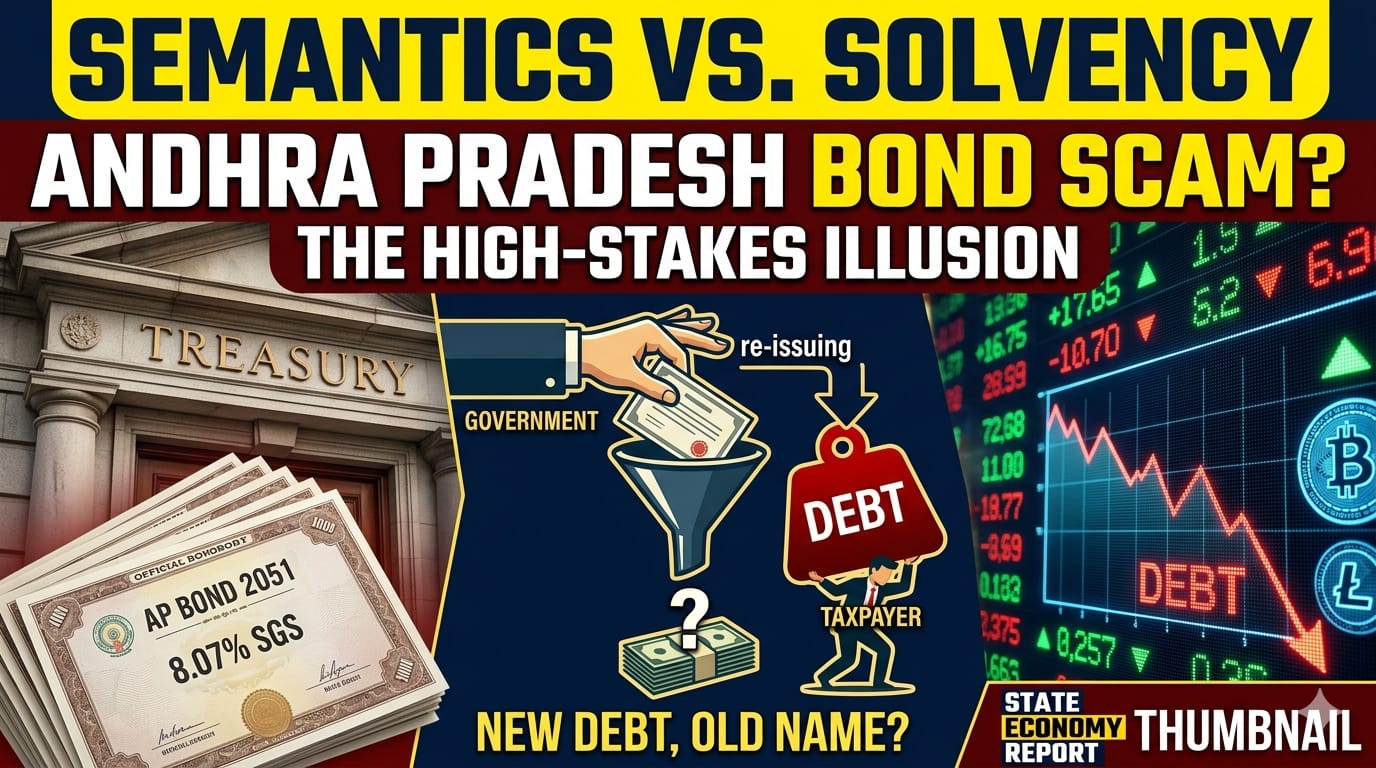

In public finance, language is often used to camouflage economic gravity. The recent notification by the Andhra Pradesh government to execute a “Re-issue of 8.07% Andhra Pradesh SGS 2051, issued on April 08, 2026” has ignited a fierce fiscal debate. While official quarters hide behind technical justifications, critics are calling out what appears to be an elaborate accounting illusion.

As an economic writer tracking state balance sheets, market trends, and fiscal policies for over two decades, I can tell you that this is not merely a routine administrative update. It is a high-stakes financial maneuver that brings the state’s structural debt management into sharp, uncomfortable focus.

The Technical Defense: Standard Procedure or Convenient Shield?

Government officials and economic advisors have been quick to dismiss public anxiety, framing the re-issue as a textbook debt management operation. Their defense rests on three pillars:

- RBI Frameworks: The administration correctly points out that re-issuing bonds is a standard practice prescribed by the Reserve Bank of India (RBI) and widely used across various state governments to manage liquidity. These fiscal operations are structured directly through official portals like the RBI Core Banking Solution (e-Kuber System), where the auction notifications are formally processed.

- Market Efficiency: Re-opening an existing bond line—like the 8.07% AP SGS 2051 increases market volume and liquidity. This makes the security attractive to institutional investors, theoretically allowing the state to capture competitive yields rather than fragmenting the market with a brand-new bond series.

- FRBM Compliance: The state maintains that all borrowings remain within the boundaries of the Fiscal Responsibility and Budget Management (FRBM) Act, backed by central clearance.

While these arguments are technically sound on paper, they act as a semantic distraction from a much harsher economic reality.

The Core Crisis: The “Not a New Security” Mirage

To argue that a re-issued bond is “not a new loan” simply because it shares the identity of an existing security is an insult to basic accounting principles. From an experienced viewpoint, the ledger tells a very different story:

The Real Impact on the State Balance Sheet

- Regarding the Bond Identity: Technically, the code remains 8.07% AP SGS 2051 (Unchanged), but the socio-economic reality is that the overall volume of this specific liability expands.

- Regarding the Exchequer Status: On paper, no new security is registered, but in reality, this represents a fresh cash inflow, meaning additional debt is acquired.

- Regarding the Total Debt Profile: While the technical nature of the liability remains the same, the state’s aggregate debt burden explicitly increases.

Regardless of the name printed on the financial instrument, fresh cash entering the treasury creates a fresh liability. Calling it a “re-issue” does not magically absolve the state from the fact that its aggregate debt mountain is growing. For retail and institutional investors tracking these public debts, updates regarding the state’s periodic market incursions can be actively verified on the RBI Retail Direct Portal, where multi-state debt expansions are transparently listed.

Shifting the Burden to 2051: Consumption Over Asset Creation

The true risk of this borrowing strategy lies in the timeline and the destination of the capital. With a maturity date locked in at the year 2051, the state is deferring its financial repayment obligations by a quarter of a century. We are essentially writing checks that the next generation of taxpayers will be forced to cash.

Deferring debt is a valid strategy only if the borrowed capital is injected into high-yielding infrastructure projects, industrial corridors, or asset creation that generates future revenue. However, serious concerns remain that these multi-crore borrowings are being consumed by non-productive spending specifically day-to-day administrative expenses, populist welfare schemes, and servicing the interest on older loans. Using long-term, 25-year debt to fund short-term consumption is a dangerous path toward structural insolvency.

The Verdict: Radical Transparency is No Longer Optional

Borrowing is a normal mechanism of modern macroeconomics, and operating on deficit budgets can stimulate growth when managed wisely. However, public trust breaks down when borrowing is shrouded in technical jargon and expenditure ambiguity.

If the government wishes to protect its debt management from political crossfire, it must move past semantic arguments. The state needs to publish a comprehensive White Paper detailing exactly where every single rupee from the 8.07% AP SGS 2051 re-issue is being deployed.

The political noise surrounding this bond will eventually fade. What will remain and what will ultimately dictate Andhra Pradesh’s economic survival is whether this capital was used to build a productive economy, or if it was simply used to keep the state afloat for another fiscal quarter.